.png?width=1200&height=600&name=Untitled%20design%20(81).png)

HR

.png?width=1200&height=600&name=Untitled%20design%20(64).png)

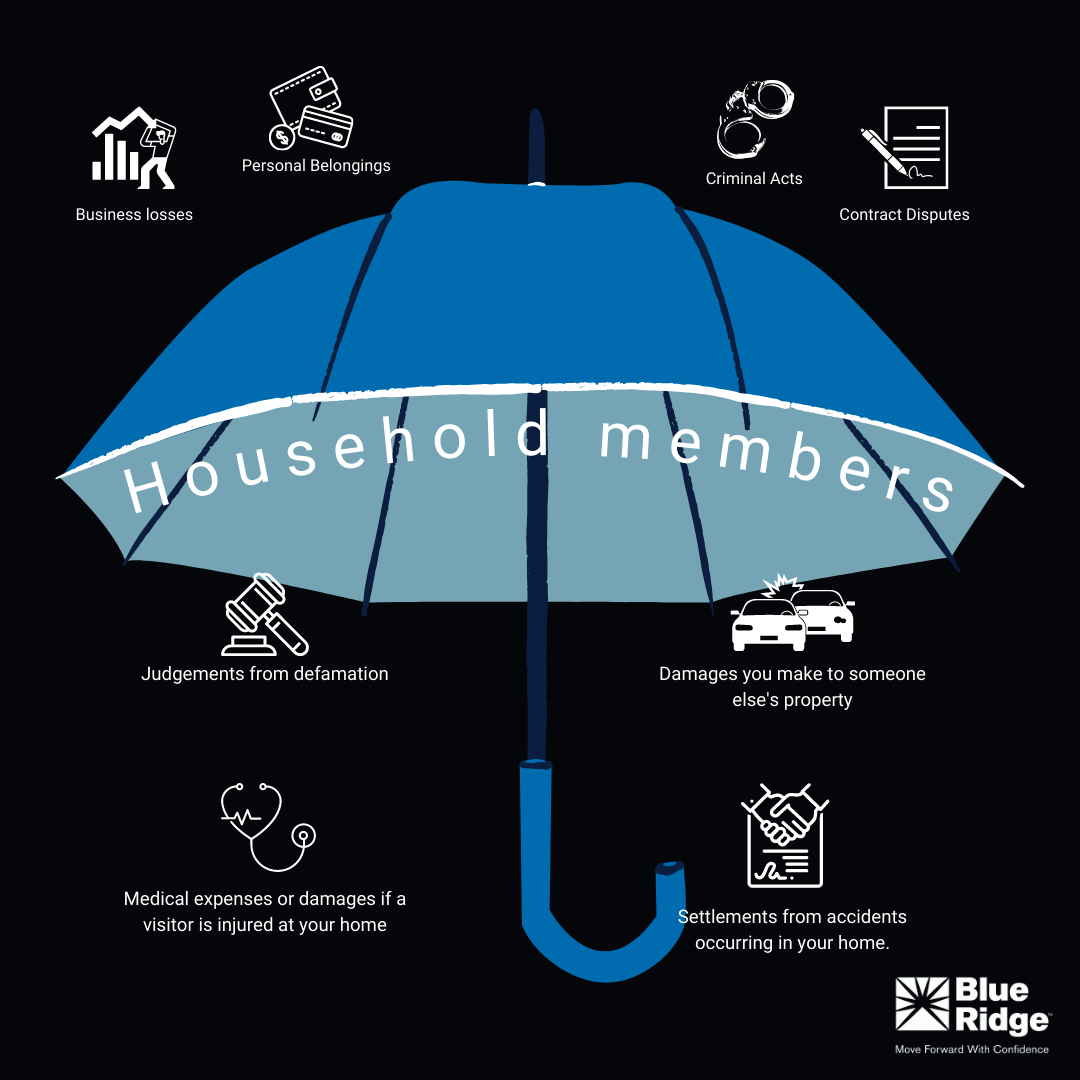

Umbrella insurance is a type of personal liability insurance that provides extra coverage beyond the limits of your standard homeowners', auto, or boat insurance policies to protect your assets from major lawsuits.

Think of this as a backup shield for your finances. When an unexpected incident occurs and your primary policy's liability limit is completely exhausted, your umbrella policy kicks in to cover the remaining balance.

Primary Policy Maxed Out: Your auto insurance pays up to its policy limit (ex. $300,000)

Property Owners: Wealth built up in your home equity can be targeted in a personal injury lawsuit.

To help you understand exactly what is protected, review this breakdown of standard coverages and common exclusions:

| What It Covers | What It Excludes |

|

Excess Bodily Injury Liability (e.g., severe multi-car accidents or guest injuries) |

Your Own Injuries or damage to your personal property |

| Property Damage Liability (e.g., accidental major damage to a neighbor's structure) | Business Liability or professional malpractice claims |

| Personal Injury Lawsuits (e.g., slander, libel, or false arrest claims) | Intentional Criminal Acts or deliberate harm |

| Legal Defense Fees (lawyers, court costs, and settlement fees from the first dollar) | Written Contract Breaches or assumed business liability |

A standard $1 million umbrella insurance policy typically costs between $150 and $300 per year, making it one of the most cost-effective ways to secure massive financial protection.

Because an umbrella policy acts as secondary coverage, the risk to insurance carriers is lower, which keeps your premium highly affordable. The exact price depends on your location, the number of properties you own, the number of properties you own, the number of vehicles you operate, and how many drivers are in your household.

Q: What does umbrella insurance actually do?

A: Umbrella insurance provides an extra layer of liability coverage that kicks in after the liability limits on your standard auto, homeowners, or watercraft insurance policies are completely exhausted.

If you are sued for a major accident, your primary pays out first. Once that policy hits its maximum limit, your umbrella policy covers the remaining balance, protecting your personal savings and future earnings from being seized to pay a judgement.

Q: How much umbrella insurance do I need?

A: You should buy enough umbrella insurance to equal your total net worth, including your home equity savings, investments, and a portion of your future income stream.

The standard starting point for most households is $1 million policy. However, if your total assets exceed $1 million, or if you have high exposure risks like a swimming pool, rental properties, or teenage drivers in the household, you should scale your coverage upward to match your full financial exposure.

Q: Does umbrella insurance cover my own property damage?

A: No, umbrella insurance does not cover your own physical injuries or damage to your personal property; it exclusively covers your legal liability to pay for damages caused to others.

For example, if your crash your car into a guardrail, your umbrella policy will not pay to fix your vehicle. However, if you cause a multi-car accident and are sued for $1 million in medical bills by other drivers, your umbrella policy will step in to cover those legal costs and damages.

Q: Why should I get umbrella insurance with an independent agency like Blue Ridge Risk Parters?

A: An independent agency can shop your coverage across multiple insurance carriers simultaneously to find the highest liability limits at the most competitive annual premium rates.

Because an umbrella policy requires you to maintain specific underlying liability limits on your auto and home insurance, our team ensures there are zero coverage gaps between your primary policies and your umbrella shield. We customize the policy to fit your specific asset profile, ensuring your financial footprint is fully protected.

Secure Your Financial Peace of Mind Today

Protecting your hard-earned assets requires proactive planning. At Blue Ridge Risk Partners, our dedicated team helps you analyze your current liability exposure and pairs you with the ideal policy to keep you fully covered.

Interested in learning more? Reach out to Sharon Meadows today.

.png?width=1200&height=600&name=Untitled%20design%20(79).png)